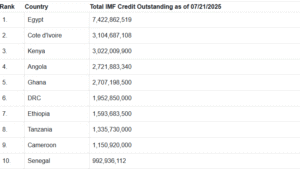

Kenya has emerged among the top 10 African countries with the highest debt burdens to the International Monetary Fund (IMF), according to the latest data from July 2025, highlighting the East African nation’s growing reliance on international financial assistance amid mounting economic pressures.

The revelation comes as the IMF continues to grapple with Africa’s escalating debt crisis, with several countries showing increased borrowing levels compared to previous months.

Kenya’s inclusion in this concerning list underscores the broader challenges facing African economies as they navigate post-pandemic recovery while dealing with global inflation, currency pressures, and reduced fiscal space.

Recent IMF activities across the continent paint a sobering picture of Africa’s financial landscape.

Egypt, which tops the regional debt rankings, recently received $1.2 billion after completing the fourth review of its $8 billion loan programme, bringing total disbursements to $3.5 billion.

However, the IMF has warned that Egypt faces “high sovereign stress,” with external debt projected to balloon from $162.7 billion in 2024/25 to over $202 billion by 2030.

Ethiopia’s situation further illustrates the continent’s debt challenges.

The country secured $262 million following a programme review but remains in delicate financial territory, currently negotiating to restructure $8.4 billion in debt with official creditors under the G20’s Common Framework while preparing to repay a $1 billion Eurobond.

The dual burden of IMF loans and commercial debt continues to strain national budgets across Africa, forcing governments to redirect resources from growth-oriented projects toward debt servicing.

This pattern threatens to undermine long-term development goals and economic transformation efforts that many African countries desperately need.

Senegal’s recent experience serves as a cautionary tale for the region.

The West African nation saw its IMF disbursements halted after officials admitted to underreporting debt levels, forcing a revision of the debt-to-GDP ratio from 74% to over 100%.

The revelation prompted S&P to downgrade the country, and IMF support remains suspended pending a credible recovery plan.

In its July 8 analytical note titled “How to Stabilise Africa’s Debt,” the IMF emphasized that sustainable debt management requires stronger institutions, growth-friendly fiscal reforms, and macro stability supported by the fund’s programmes.

However, critics argue that IMF assistance often comes with strict conditionalities and austerity measures that limit countries’ ability to pursue domestic priorities and can undermine public confidence.

For Kenya, joining this list of heavily indebted nations signals the urgent need for comprehensive debt management strategies and fiscal reforms.

The country, like many of its continental peers, must balance immediate financial stability needs with long-term economic development objectives while avoiding the dangerous cycle of perpetual borrowing and repayment that has trapped several African economies.

As African governments continue to seek IMF support to navigate economic headwinds, the challenge remains finding sustainable pathways to growth that don’t compromise future generations’ economic prospects through unsustainable debt accumulation.

{kind=link}